Belgique

Belgique

España

España

France

France

Germany

Germany

India

India

Italia

Italia

Netherlands

Netherlands

Polska

Polska

Portugal

Portugal

Suisse

Suisse

United Kingdom

United Kingdom

United States

United States

Health Insurance for Freelancers in the Netherlands: What You Need to Know

- Key takeaways

- Overview of health insurance for freelancers in the Netherlands

- What should freelancers know about health insurance?

- Estimated health insurance costs for Freelancers in 2026

- What is included in health insurance for freelancers?

- How to get health insurance for a freelancer?

- How Hightekers supports freelancers in the Netherlands

- Final thoughts

- Frequently asked questions

Health insurance isn’t just a smart move for freelancers in the Netherlands—it’s the law. For every self-employed professional, from consultants in Amsterdam to digital nomads in Rotterdam, securing a Dutch health insurance policy is an important first step. This system is designed to guarantee you access to the country’s high-quality medical care while protecting you from financial ruin should you fall ill.

Unlike in some countries where coverage is tied to an employer, the Dutch model places the responsibility squarely on the individual. This guide cuts through the complexity, explaining exactly what you need, what it covers, and how to arrange it correctly from day one.

Key takeaways

- Health insurance is legally mandatory for all residents and freelancers in the Netherlands.

- Compare your health insurance options for freelancers annually, as insurers compete on price.

- Your total cost includes a monthly premium, a standard annual deductible, and income-based tax.

- You can switch providers each December for better self employed health insurance deals.

- Working with an employment partner like Hightekers can simplify compliance and access to mandatory health insurance for freelancers.

Overview of health insurance for freelancers in the Netherlands

The cornerstone of the Dutch system is the Zorgverzekeringswet (Healthcare Insurance Act). This law mandates that everyone who lives or works in the Netherlands must take out at least a basic health insurance policy (basisverzekering).

This includes:

- Freelancers

- Independent contractors

- Self-employed professionals

That’s regardless of whether you have a Dutch employer.

This isn’t a suggestion, but a legal requirement. The system operates on a unique public-private model. The government defines the exact package of essential care that every insurer must provide, ensuring a universal standard.

Private insurance companies then administer these policies, competing on price, customer service, and optional add-ons. This structure balances social solidarity with market efficiency, but for freelancers it means one thing: you must actively choose and purchase a policy.

Importance of being insured

Failing to do so has real consequences. The Central Administration (CAK) actively pursues uninsured residents, issuing warnings followed by substantial fines. If you continue to refuse, they can enrol you in a policy by force and deduct the premiums from your income.

Beyond avoiding penalties, being insured is your ticket to a seamless healthcare experience. It allows you to register with a local doctor, access hospitals, and receive prescribed medications without facing thousands of euros in out-of-pocket costs.

What should freelancers know about health insurance?

Understanding the rules and costs is crucial for budgeting and compliance. Here’s what every self-employed professional must know.

The mandatory basics: Deadlines and penalties

Once you become a resident or start your freelance business, you have a four-month registration window to take out insurance. If you apply within this period, your coverage can be backdated to your arrival or start date.

Miss this deadline, and your policy will only begin from your application date, potentially leaving you with a costly gap.

As noted, the CAK enforces this rule and there are very few exceptions. Individuals with documented conscientious objections based on faith may apply for an exemption. However, they must pay an equivalent amount in extra taxes. For the vast majority, securing self-employed health insurance is an immediate priority.

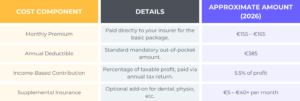

Breaking Down the Costs: What You Actually Pay

As a freelancer, you handle all contributions yourself of health insurance for the self-employed. Your total cost has three components:

- Monthly premium: This is the fee you pay directly to your chosen insurer. For the basic package in 2026, this typically ranges from €155 to €165 per month. You can lower this premium by opting for a higher annual deductible.

- Annual deductible (Eigen Risico): This is a mandatory out-of-pocket amount you pay each year for certain treatments before your insurer covers the rest. The standard deductible in 2026 is €385. You can voluntarily increase this to a maximum of €885 to reduce your monthly premium. That’s a common tactic for healthy freelancers who rarely visit the doctor.

- Income-based contribution (Inkomensafhankelijke Bijdrage): This is a separate contribution calculated as a percentage of your taxable profit (roughly 5.5% in 2026, up to a maximum annual amount). Unlike the monthly premium, this is not paid to your insurer. It is calculated annually by the Dutch Tax and Customs Administration (Belastingdienst) and collected through your income tax assessment.

Estimated health insurance costs for Freelancers in 2026

Here’s a table to summarise the costs in 2026:

What is included in health insurance for freelancers?

The government-defined basic package is comprehensive, covering all medically necessary care. Every insurer provides the same core benefits, which include:

- Visits to the family doctor: Consultations with your GP (huisarts) are fully covered, with no deductible applied. They are your primary point of contact for referrals to specialists, prescriptions, and non-urgent medical advice, forming the backbone of Dutch primary care.

- Hospitalisation: This includes necessary hospital stays, surgical procedures, treatment by medical specialists, and all associated medical costs incurred within a hospital setting. Coverage is subject to your chosen annual deductible amount for the treatments provided.

- Psychological care: The basic package includes essential mental health support, such as sessions with a psychologist or psychiatrist for diagnosed conditions. There may be limitations on the number of sessions. Also, a referral from your GP is typically required to access this care.

- Pregnancy, childbirth, and newborn care: Nearly all care related to maternity is covered, from midwife appointments and hospital deliveries to postnatal home visits (kraamzorg) and care for your newborn. These services are exempt from the annual deductible.

- Emergency care: Coverage includes urgent medical assistance, such as ambulance transportation and treatment received at a hospital’s Accident & Emergency (A&E) department. This ensures you are protected in acute situations without facing prohibitive costs.

- Prescription drugs: Medications prescribed by your doctor or a specialist are included in the basic package. You may pay the full cost upfront and then claim reimbursement, or simply pay a pharmacy charge, depending on your insurer’s policy.

It’s important to note that GP visits and maternity care are exempt from the annual deductible.

Supplemental insurance: Covering the gaps

While the basic package is robust, it excludes some common healthcare needs. This is where optional supplemental insurance (aanvullende verzekering) comes in. You can add this coverage to your policy, typically at the start of each new calendar year.

Common and valuable add-ons for freelancers include:

- Adult dentistry: This covers routine check-ups, teeth cleaning, fillings, and sometimes more complex procedures like root canals or crowns. Coverage is usually up to an annual maximum amount, with policies varying significantly in their reimbursements.

- Physiotherapy: Essential for treating musculoskeletal issues, this covers treatments for chronic conditions or recovery after an accident. Basic insurance only covers limited physio for specific chronic issues, making supplemental cover vital for active professionals.

- Optics: This provides a contribution towards the cost of prescription glasses, contact lenses, or laser eye surgery. Most policies offer an allowance every one to three years, with the amount depending on the level of cover you select.

- Additional care for pregnant women: Beyond the basic midwife care, this can cover extra postnatal home help, breastfeeding support, or complementary therapies. It provides greater flexibility and support during the maternity period.

Unlike basic insurance, insurers can refuse supplemental coverage based on your health or ask medical questions. However, it’s important since freelancers don’t get sick leave in the Netherlands like employees.

When is Dutch health insurance not required?

While the rule is strict, there are limited scenarios where you might not need a Dutch policy immediately:

- Short-term stays: If you are visiting temporarily (for example, as a tourist or for a brief project), you can rely on your European Health Insurance Card (EHIC) or private travel insurance.

- Foreign-based business: If your company and tax residence are firmly outside the Netherlands and you only spend short periods in the country, you may remain under your home country’s system. The Dutch Social Insurance Bank (SVB) can provide a definitive ruling.

- Awaiting registration: If you have moved but do not yet have a BSN or residence permit, you cannot yet sign up for Dutch insurance. In this interim period, a temporary expat health insurance policy is a vital stopgap to ensure you are not left uncovered.

How to get health insurance for a freelancer?

Arranging your insurance is a straightforward process once you know the steps. Follow this guide to get covered correctly regarding insurance for self employed :

1. Register your business

First, formally register your freelance business with the Dutch Chamber of Commerce. This establishes you as a legal entity and connects you to the tax authorities.

2. Obtain your BSN

Register with your local municipality (gemeente) to get your Citizen Service Number. This number is essential for all administrative procedures in the Netherlands, including applying for health insurance.

3. Compare insurers

Use independent comparison websites like Zorgwijzer.nl or Independer.nl to compare health insurance options for freelancers. All insurers offer the same basic coverage, but they differ in monthly premium, deductible options, customer service, and English-language support.

4. Apply online

Once you’ve chosen a provider, complete the online application. You will need your BSN, proof of address, and Dutch bank account details. Remember the four-month rule and apply promptly to avoid issues.

5. Register with a GP

After your policy is active, find and register with a local general practitioner. They are your first point of contact for all non-emergency medical issues and provide necessary referrals to specialists.

6. Use expat insurance as a temporary solution

If you are waiting for your KvK registration or BSN, you cannot join the public system. During this gap, a flexible expat insurance policy is a crucial temporary solution to ensure you are protected from day one.

How Hightekers supports freelancers in the Netherlands

Hightekers offers a practical employment model for freelancers who want to work compliantly in the Netherlands while maintaining their independence.

Freelancers continue to find their own clients and manage their projects, but sign an employment contract with Hightekers.

This structure allows freelancers to remain operationally independent, while Hightekers takes care of payroll, invoicing, taxes, and statutory compliance.

Because freelancers are employed by Hightekers under a Dutch contract, they can access employee benefits, such as health insurance, while avoiding the administrative burden and risks of managing everything alone.

For many self-employed professionals, this provides a balance between flexibility and stability, combining the freedom of freelancing with the security of compliant employment.

Final thoughts

Securing compliant health insurance for freelancers in the Netherlands is a non-negotiable first step. It helps establish both your legal residency and access to quality care. However, overcoming this mandatory requirement is just one part of the complex administrative burden facing self-employed professionals.

For freelancers who want greater stability, legal certainty, and peace of mind, working with Hightekers it’s a reliable option.

By employing freelancers under a compliant Dutch contract, Hightekers manages essential administrative responsibilities such as payroll, taxes, invoicing, and access to mandatory health insurance.

This allows professionals to focus fully on their work, while knowing their employment and social security situation in the Netherlands is handled correctly and transparently.

Discover how Hightekers supports freelancers in the Netherlands

Frequently asked questions

Can I use my home country’s health insurance instead of Dutch insurance?

This depends on your residence and tax status. If you live and pay taxes in the Netherlands, you must have Dutch insurance.

If your main residence and business are abroad, you may remain under your home system. The SVB can provide a binding decision.

Can I switch my health insurer later?

Yes, you can change your insurer once per year. The switching period runs through December, and you must cancel your old policy by the 31st of December. Your new policy will then start on the 1st of January of the coming year.

Do I need additional liability insurance as a freelancer?

While not legally required like health insurance, professional liability insurance (BAV) is highly recommended. It protects you from financial claims if a client suffers loss due to your advice or work. Many clients and platforms require it as a condition for contracts.