Belgique

Belgique

España

España

France

France

Germany

Germany

India

India

Italia

Italia

Netherlands

Netherlands

Polska

Polska

Portugal

Portugal

Suisse

Suisse

United Kingdom

United Kingdom

United States

United States

Tax Residency in Spain: What Freelancers and Expats Need to Know

- Key takeaways

- Tax residency rules in Spain: When do you become a resident?

- Understanding the standard Spanish income tax system

- What is the Beckham Law and who can benefit?

- Double taxation agreements: Avoiding being taxed twice

- Social security obligations for expats in Spain

- When to hire a tax advisor

- How Hightekers can help freelancers

- Final thoughts

- Frequently asked questions

Spain, with its vibrant culture and enviable lifestyle, is a top destination for freelancers across Europe and beyond. However, a clear blue sky and Mediterranean beaches come with a legal framework that requires your attention, especially regarding tax residency.

Dealing with this system is crucial, not just for compliance, but to make informed financial decisions for your new life.

This guide will walk you through Spain’s residency rules, the special benefits you might access, and how to avoid being taxed twice. Whether you’re a freelancer relocating to Spain, a consultant working remotely with foreign clients, or a professional managing international income.

Key takeaways

- Your physical days in Spain determine your tax residency status.

- Residents pay Spanish income tax on worldwide earnings; non-residents do not.

- Use the Beckham Law for a flat 24% tax rate on employment income.

- Double taxation treaties protect your income from being taxed in two countries.

- Always seek expert advice on residency from services like Hightekers

Tax residency rules in Spain: When do you become a resident?

Your entire Spanish income tax liability hinges on a single determination: whether Spain considers you a tax resident. For freelancers living in Spain, this status determines how all income — whether from Spanish or international clients — is taxed.. Spain uses clear, objective tests, and you are considered a resident for tax purposes if you meet any of the following criteria:

- The 183-day rule: You spend more than 183 days in Spain during a calendar year. It’s vital to note that temporary absences are counted unless you can prove tax residency in another country. This makes Spain an attractive base for digital nomads, but also a potential tax home if you’re not careful with your time.

- The centre of economic interests: Your primary base or the core of your professional or economic activities is in Spain. For example, if you are a consultant living in Portugal but derive 80% of your income from managing a Spanish startup, you could be deemed a Spanish tax resident.

- The family ties presumption: If your spouse (not legally separated) and dependent minor children permanently reside in Spain, you are presumed to be a tax resident there yourself. This can be a critical factor for families where one partner moves ahead of the others.

A key concept in the Spanish tax system is that there is no “part-year” resident status. You are either a full resident or a non-resident for the entire tax year. Once you cross the threshold, you are taxed in Spain on your worldwide income.

That’s from your salary in Madrid to rental income on a flat in Berlin or dividends from investments in London. Non-residents, in contrast, are only taxed on income generated within Spain.

Understanding the standard Spanish income tax system

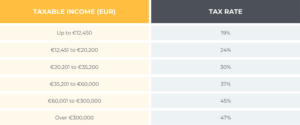

As a tax resident, you will pay Spanish income tax (Impuesto sobre la Renta de las Personas Fisicas, or IRPF) on your global earnings. Spain uses a progressive tax system, meaning your rate increases with your income level.

The rates are composed of a national scale plus an autonomous regional scale, which can vary significantly.

Here’s a table showcasing the tax rate:

Investment income (like dividends, interest, and capital gains) is taxed under a separate “savings” scale, with rates from 19% to 30%. Residents must also consider other potential taxes, such as the annual Wealth Tax on worldwide net assets above a high threshold. This varies by region (for instance, it is not levied in Madrid).

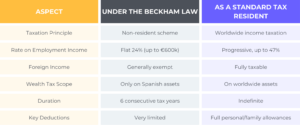

What is the Beckham Law and who can benefit?

To attract international talent, Spain offers a powerful incentive officially known as the Special Tax Regime for Inbound Workers, colloquially called the Beckham Law. This regime allows eligible individuals to be taxed as non-residents for a period, even while living in Spain. It typically applies to employees relocating to Spain or certain remote workers employed by foreign companies.

The core benefit is a flat tax rate of 24% on Spanish-sourced employment income up to €600,000 (income above this is taxed at 47%). Crucially, your foreign income—be it a UK government pension, rental property in France, or stock dividends from a Dutch company—is generally exempt from Spanish taxation during the regime’s term.

Beckham Law vs. standard tax residency

Eligibility has been broadened and now includes not only employees of Spanish companies but also remote workers and digital nomads who move to Spain for a job with a foreign company.

However, you must not have been a Spanish tax resident in the previous five years, and you must apply using Form 149 within six months of starting your work or registering with Social Security.

Double taxation agreements: Avoiding being taxed twice

A primary concern for any expat is double taxation Spain—the risk of paying income tax on the same money to two different countries. Spain has an extensive network of Double Taxation Treaties (DTTs) with over 90 countries. This includes all EU member states, the UK, the United States, and Canada.

These treaties contain “tie-breaker” rules to determine a single country of tax residency for individuals who might otherwise be claimed by two nations. Consultants working remotely for international companies should be aware of the relevant rules.

The rules typically examine factors like:

- Your permanent home

- Centre of vital interests (personal and economic ties)

- Habitual abode

- Nationality

For instance, a German executive living in Barcelona but with a permanent home and family in Hamburg might be found to have stronger ties to Germany under the treaty. More importantly, DTTs provide mechanisms to eliminate double taxation. That’s usually by allowing you to claim a credit in your country of residence for taxes paid in the source country.

Social security obligations for expats in Spain

Social security is separate from income tax and determines your access to Spain’s public healthcare, pensions, and unemployment benefits. If you are employed by a Spanish company, you and your employer will make mandatory contributions.

The situation becomes more nuanced for those working remotely for a foreign employer or as freelancers. Within the EU/EEA and Switzerland, regulations determine which country’s system you contribute to. That’s generally the country where you perform your work.

For other nationalities, like Americans or Britons post-Brexit, Totalization Agreements come into play. For example, the U.S.-Spain agreement prevents dual contributions and helps determine coverage. Freelancers must register and pay a monthly fee to the Spanish social security system, which starts at a reduced rate and increases with income.

When to hire a tax advisor

Given the complexity of personal tax situations, seeking professional advice is not a luxury but a necessity for many expats. Consider hiring an international tax advisor in these scenarios:

- Navigating the Beckham Law application: The application process and ongoing compliance are strict. An advisor ensures you meet deadlines (like the critical 6-month window) and correctly submit forms like Modelo 149 and the annual Modelo 151.

- Managing complex income streams: If you have multiple income sources, an advisor can optimise your position under a DTT and handle reporting like the Modelo 720 for declaring foreign assets over €50,000. For instance, a Spanish salary, UK property rental, and investment dividends from a Swiss account.

- Understanding cross-border implications: For Americans, the interplay of the Beckham Law with FTC/FEIE choices is highly complex. For Britons post-Brexit, understanding new bilateral agreements is key. An expert can model different scenarios to minimise your global tax liability.

- Facing an audit or investigation: The Spanish Tax Agency (Agencia Tributaria) is increasingly sophisticated. Professional representation is invaluable if you face an inquiry.

A good advisor provides clarity, ensures compliance to avoid penalties, and ultimately aims to structure your affairs efficiently, giving you peace of mind to enjoy your life in Spain.

How Hightekers can help freelancers

Managing international freelance income doesn’t have to mean overcoming complex bureaucracy alone. You’ll find that Hightekers offers a streamlined structure which handles the heavy lifting while you focus on your work.

Here are some of the ways Hightekers can help:

- Work with international clients: Keep your client relationships exactly as they are—you find your own projects and set your rates. Meanwhile, Hightekers handles multi-currency invoicing and global payments on your behalf.

- Remain compliant with tax and social security rules: Local experts manage country-specific tax filings, social security contributions, and regulatory requirements.

- Simplify administration: No more invoices, tax returns, or chasing late payments. Your personal dashboard tracks everything.

- Combine freelance flexibility with employment security: You sign a permanent employment contract with Hightekers, gaining benefits like sick pay, holiday pay, and pension contributions. However, you still maintain complete independence over your projects

For freelancers seeking a smarter way to work across borders, Hightekers transforms administrative complexity into simplicity. Overall, it allows you to earn more, worry less, and focus entirely on what you do best.

Final thoughts

Dealing with Spain’s tax residency rules is only half the battle—the real challenge lies in structuring your cross-border work correctly from day one. For freelancers relocating to Spain, getting this wrong can mean unexpected tax bills or social security gaps.

For consultants working internationally, each client relationship brings potential compliance landmines. This is where services like Hightekers prove valuable.

We’ll offer administrative support by handling invoicing, multi-country tax compliance, and social security contributions while providing employment benefits. Whether you’re basing yourself in Barcelona or consulting across European borders, proper structuring ensures you remain compliant

Contact us to learn more about Spain’s tax residency rules

Frequently asked questions

How are the 183 days counted?

The 183 days include every day you are physically present in Spain, and temporary absences count. Your day of arrival and departure are both considered full days.

To exclude days, you must prove formal tax residency in another jurisdiction with a certificate of residence.

Can I be a tax resident in two countries?

Yes, under each country’s domestic laws. However, the double tax treaty between Spain and the other country will include ‘tie-breaker’ rules to assign you a single tax residency for the purposes of the treaty. This prevents double taxation in Spain on the same income.

What is the Modelo 720?

This is an informational declaration for Spanish tax residents holding certain assets outside Spain valued over €50,000 per category (accounts, securities, property). Failure to file or inaccuracies can result in significant penalties, even though it is not itself a tax payment.

Do I pay Spanish tax on my foreign pension?

As a tax resident, your worldwide income is taxable in Spain, which includes foreign pensions. However, the applicable double taxation treaty may grant exclusive taxing rights to the pension’s source country, or Spain may tax it but grant a credit for foreign tax paid.

How does the Beckham Law affect my family?

Your spouse and children under 25 can be included in your application. They will also benefit from the special regime, meaning their Spanish-source income is taxed at the flat 24% rate. That’s provided they become tax residents in Spain and are not independently wealthy.

What happens if my remote employer doesn’t set up Spanish payroll?

You risk severe non-compliance. You may be held personally liable for unpaid social security and tax.

Furthermore, your employer could face fines and be deemed to have created a permanent establishment in Spain, making its global profits subject to Spanish corporate tax.

When do I need to file a Spanish tax income return?

Residents file the annual declaration (Modelo 100) between April and June. Also, non-residents with Spanish-sourced income must file quarterly using Modelo 210. The first return is due in the calendar quarter immediately following the accrual of the taxable income.